In most sovereign nations, sub-soil minerals are owned by the state. The minerals are a part of the “commons” — assets owned ultimately by the citizens. The problem we face is that the IMF, UN & IPSASB standards for government accounting, statistics and disclosure treat receipts from minerals as “windfall revenues” rather than “capital receipts on account of the sale of a non-renewable natural resource asset.” This is a major accounting anomaly, similar to the funding of pension liabilities on a pay-as-you-go basis, but with even bigger and more dangerous implications. Politicians love this error as it enables government spending without having to raise taxes. The World Development Indicators show that the total energy and mineral depletion that occurred between 1970 and 2013 amounts to $27 trillion. Much of the receipts from this has been already spent or consumed, aided in part by government accounting for mineral receipts as revenues instead of their actual status — sale of assets.

Politicians love to spend money, but hate raising taxes. An important accounting metric for evaluating the performance of government entities is revenues minus expenses, the revenue surplus / deficit or the Net Operating Balance (NOB). An entity constantly incurring deficits is not in a position to sustain its operations in the long term. At some point, it would have consumed its capital, and creditors would stop financing the deficit, resulting in a crisis. Consequently, there are great incentives for politicians to overstate revenues and understate expenses, thereby understating the deficit.

One recent instance is the pay-as-you-go accounting for pensions. Since pension liabilities were not recognised as expenses when incurred, politicians were happy to promise greater benefits, as there was no immediate impact on the budget deficit. The consequence was a ballooning of unrecognised pension liabilities that would have to be paid in future. Many countries have moved to defined contribution pensions in recognition of the skewed incentives to understate pension liabilities.

Goa Foundation (GF), a non-profit in India, has pointed out in a note, sent to the IMF and other global standard setters, and in a subsequent response to FAQs, that a similar anomaly, perhaps larger, is created by the treatment of mineral receipts as revenues.

The problem

Most accountants would agree minerals are a shared inheritance, akin to family gold. Royalties are clearly the consideration for the sale of the minerals, a capital receipt. However, IMF’s Government Finance Statistics Manual 2014, the global standard for public finances, treats mineral receipts as property income, specifically rents. The accounting needs changing.

The impact is two-fold. First, mineral receipts are treated as revenue. More revenues are good. Politicians are incentivized to extract till nothing is left — see Nauru or the Arctic Refuge.

Second, minerals are being sold for much less than its true value. IMF estimates that the best case is a 15% loss in value when selling oil, and 35% for minerals. Since mineral receipts are treated as revenue, the loss in asset value is not recognised in the government accounts. This incentivizes crony capitalism as there is no disclosure of any losses in value.

Goa example

In iron ore mining in Goa, over an 8 year period (2004–2012), the loss is estimated at over 95% of the economic rent (sale price minus all expenses and a generous profit). In other words, for iron ore worth 100 (after all extraction costs), the government of Goa as owner received less than 5.

The majority of the value (60%) was captured by miners, while a part was captured by the national government (35%). This is simply a transfer of wealth from the commons to certain private individuals, and is astonishing for its scale – an average of 22.8% of GDP was redistributed upwards each year.

Two large errors

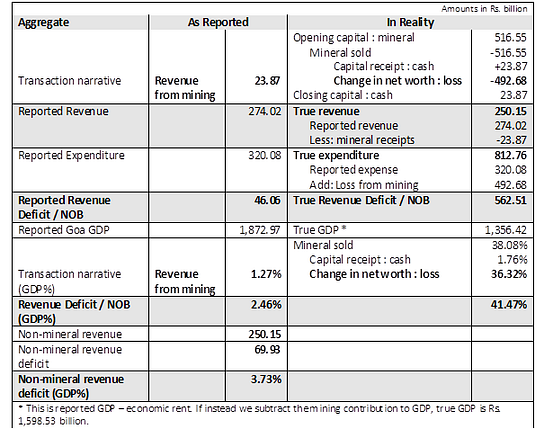

In absolute terms, minerals worth Rs. 516.55 billion (economic rent) were exported, and the state of Goa received merely Rs. 23.87 billion. It recognised the receipt as “revenue”, and simultaneously ignored the reduction of the asset of Rs. 516.55 billion (or a net loss of Rs. 492.68 billion.)

Incorrectly treating the mineral receipts as “revenue” creates an incentive for more extraction — more mining = more revenue (Rs. 23.87 billion). If we simply treated this as a capital receipt, incentives for extraction reduce — more mining doesn’t impact income. However, if the loss in asset value is also recognised as an expense, then mining on poor terms is less likely — more mining = larger losses (Rs. 492.68 billion).

Impact on Goa’s public finances

Mineral receipts were reported at merely 8% of government revenues, and 1.3% of GDP. This hides a catastrophe. The table below illustrates how Goa’s public finances would change with appropriate accounting for mineral receipts.

Governments usually target a balanced budget or a small deficit. The reported revenue deficit (NOB) in Goa was 2.46% of GDP, already a little high. In the present accounting framework, increasing mining would increase revenues, lowering the deficit.

The “non-mineral deficit” is an additional measure provided by the IMF. As its name indicates, this metric effectively treats mineral receipts as capital receipts by excluding them from government revenues. Goa’s non-mineral revenue deficit was 3.73% of GDP. This is already unsustainable. Observe that increasing or reducing mining has no impact on the non-mineral deficit.

However, accounting for the losses in capital as expenses, the true revenue deficit (NOB) is an astonishing 41.47% of GDP. It is unlikely that any democracy has reported such large revenue deficits in normal times. Note that additional mining worsens the deficit.

The current revenue accounting of mineral receipts is incentivising the consumption of mineral wealth across the world. This is unsustainable.

Global problem

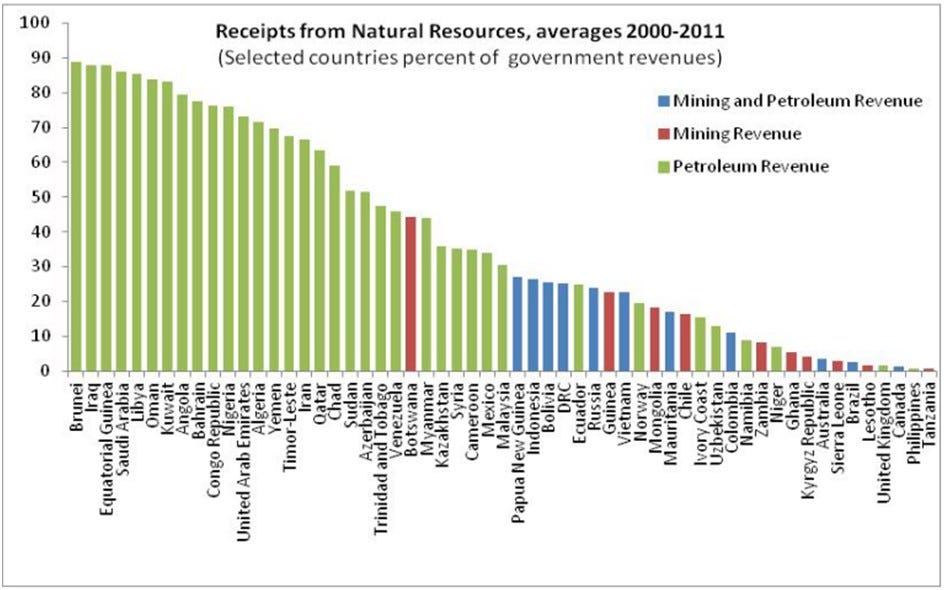

This problem is widespread. The chart below from the IMF shows how dependent resource rich governments are on “mining and petroleum revenue”. For comparison, “mining and petroleum revenue” was only 8% of Goa government’s revenues, approximately Namibia on the right of the chart.

In order to arrive at the true revenue deficit / NOB, we need to strip out all these “revenues” to arrive at the true revenue. At the extreme, since Brunei reported natural resource receipts of 88% of government revenues, its true revenues was only around 12% of what is reported. Botswana was at 55%. Goa was at 92%.

We also need to subtract the losses of mineral value. IMF estimated that losses of 15–35% are common in oil, and 35–55% in minerals. It is clear that if these losses are recognised, the government revenue deficit / NOB will balloon even further in these nations. The current system of mineral depletion and consumption of “mineral revenues” is unsustainable.

Political incentives & Consequences

The accounting treatment is driving perverse incentives. Politicians argue for new mines or increased extraction on the grounds of a boost to the government revenues. Since mineral receipts are accounted for as revenues, a derived goal is to maximise revenues, a fuzzy target. This drives increased extraction at lower prices, large losses, wasteful spending, declining wealth and increasing inequality.

The distressed sale of minerals incentivizes rapid mining and exit. The people on the ground & the environment are obstacles between the miner and great wealth. Often they resist, resulting in conflict and civil wars.

The commodity cycle exacerbates the problem. Government “revenue” rises when commodities boom, and expenditure does too — politicians know spending more leads to re-election. When prices crash, there are three painful choices — cut expenditure, raise taxes, or sell more minerals. Look at Venezuela. Or Alaska for a developed nation example.

If politicians had to recognize that they are selling the family gold, significant losses would be politically untenable. This would squeeze the corruption and crony capitalism. Arguments for consuming the capital would be difficult. Consequently, the savings rate is likely to rise, leading to further growth.

Solutions

Some countries on this chart have recognised the problem. Botswana explicitly targets its non-mineral budget deficit. Similarly Norway saves all its oil receipts in its famous fund, while only allowing the real income from the fund to be treated as revenue. However, the permanent solution is a simple change to IMF’s Government Finance Statistics Manual 2014. Will they?

This article was first published on the Public Finance International blog. This version is an edited, rearranged & expanded version of the article.

Read more:

Mitigating the Resource Curse by Improved Government Accounting: Goa Foundation’s note to the IMF and others explaining this issue, and how metaphors used are exacerbating the problem

FAQs on Accounting Metaphors: A response to various comments received to the previous note.

What is The Future We Need: a summary of our broader campaign. Highly recommended.

Stop selling the family farm: How the Arctic Refuge has been opened to oil drilling, partly due to this issue.

Alaska’s Budget Problem: How “revenue” accounting, commodity volatility and a fiscal rule that only 25% be saved in the Permanent Fund has caused the ongoing budget crisis that started in 2013.

Goa Foundation’s representation on India’s National Mineral Policy. It gives a holistic view of the changes needed as far as managing mineral wealth goes, although it is India centric, and builds on the existing policy.

Rahul Basu is the Research Director of Goa Foundation, an environmental NGO in India. The Future We Need is a global movement asking for natural resources to be viewed as a shared inheritance we hold as custodians for future generations. This work is based on the practical work of the Goa Foundation.