Minerals are inherited wealth, usually owned by the state. The goal must be to keep capital at least constant — consuming capital is unsustainable, a failure of stewardship. Extraction is effectively the sale of the mineral wealth, with the consideration being the royalty, production shares, signing bonus, etc that the government receives as mineral owner. As minerals are wealth, the consideration is capital in nature. Unfortunately, for government finance statistics, the consideration is called “Rent”, and classified as “Revenue”. The eventual consequence is the consumption of the wealth inheritance. This article is based on three fairly recent studies by the IMF that demonstrate clearly how public sector wealth is declining in resource-rich nations — six Gulf nations, the UK and Norway.

Gulf Cooperation Council (GCC) Countries

GCC comprises Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the UAE. The IMF report, “The Future of Oil and Fiscal Sustainability in the GCC Region” (Mirzoev et al, 2020) was released recently. From the abstract:

“At the current fiscal stance, the region’s financial wealth could be depleted by 2034. Fiscal sustainability will require significant consolidation in the coming years. Its speed is an intergenerational choice. Fully preserving current wealth will require large upfront fiscal adjustments. More gradual efforts would ease the short-term adjustment burden but at the expense of resources available to future generations.”

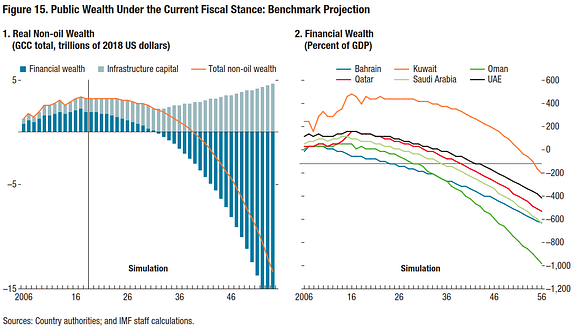

The report makes clear that the Gulf states are unsustainable. The chart below shows the non-oil Primary Balance, defined in the GFSM as “Total revenue excluding natural resource-related revenue minus total expense excluding natural resource-related expense”, and “excluding interest expense”. All states have a non-oil Primary deficit of over 10% of GDP, and at the worst end, over 100% of GDP (Kuwait in 2012).

The report looks at likely projections for oil “revenue”, the wealth of the nations and the projected fiscal part, and found

“In illustrative simulations, long-term fiscal sustainability in the GCC requires the average non-oil primary fiscal deficit to decline from the present level of 44 percent of non-oil GDP to mid-single digits by 2060.”

As the charts show, under the benchmark projections of the IMF, non-oil wealth rapidly goes negative. Keep in mind that simultaneously, the oil wealth in the ground is being extracted and depleted. In effect, the GCC countries are on the path to bankruptcy. A strange fate for nations with such large oil endowments. And the only options are painful.

“ … Continued economic diversification will be important but would not suffice on its own. Countries will also need to step up their efforts to raise non-oil fiscal revenue, reduce government expenditure, and prioritize financial saving when economic returns on additional public investment are low. … The intergenerational distribution of wealth would be helped by an early start. Gradual fiscal adjustment would ease the burden on the current generation, but the size of required fiscal consolidation would be made larger and its burden transferred onto future generations who would inherit a lower stock of wealth. A notion of the level of wealth that countries intend to leave to future generations would help anchor their long-term fiscal strategies.

“For all generations to equally share the initial level of wealth, the nonhydrocarbon fiscal balance must be immediately improved to a level that is consistent with keeping wealth constant over time. The magnitude of the estimated adjustment is large, averaging 32 percent of nonhydrocarbon GDP or more than double the fiscal adjustment achieved by the GCC region during 2015–18. The benefit of preserving initial wealth is that its larger stock generates higher dividend income which, in turn, creates additional fiscal space in the future.

“The biggest challenge will be managing the broader economic transition. The long-term future of oil outlined in this paper would have a multitude of socioeconomic consequences affecting employment, household incomes, and business confidence and investment. More work is needed to fully understand these consequences, design mitigation strategies, and build the social consensus required for their implementation.”

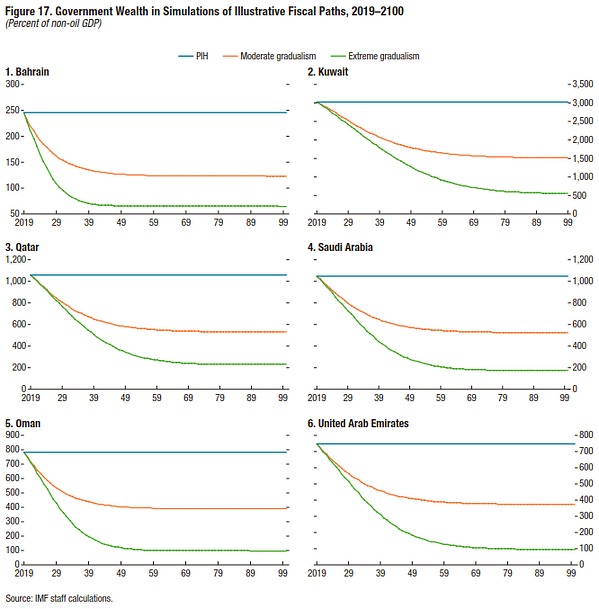

The IMF also examines three different scenarios. The PIH option is when this entire fiscal adjustment takes place now. That’s the ideal but impossible scenario. The moderate gradualism probably represents what the IMF hopes will happen, and extreme gradualism a more real picture. The different between the PIH line and what will actually be achieve is the amount of intergenerational wealth that is being consumed. If we look at Bahrain, between PIH and extreme gradualism, approximately 230% of GDP in terms of wealth will have been consumed.

The United Kingdom

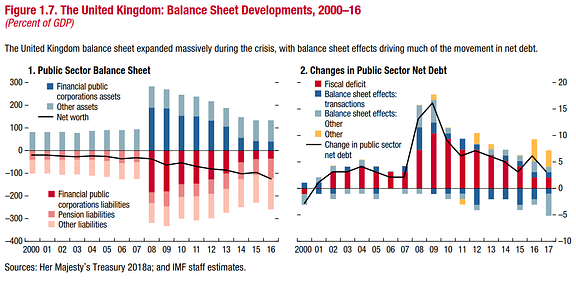

The United Kingdom with exploiting a massive coal endowment, boosted itself through colonialism, and finally there was the North Sea oil endowment. Stewardship would suggest that the present generations of United Kingdom would have inherited an exceptionally strong balance sheet.

Two credible studies of UK’s management of its North Sea oil endowment indicate that between 35 & 39% of the value of the North Sea oil was lost. (Note the value was calculated after extraction costs and a reasonable profit.) However, the balance 61–65% did reach the budget. What happened?

It is surprising to find that IMF’s October 2018 Fiscal Monitor: Managing Public Wealth reports that the UK public sector net worth is approximately -125% of GDP. And the trend is negative. Put simply, the entire mineral endowment plus the gains from colonialism has been squandered, and the government has gone even further into debt. Difficult to imaging that the UK recently ruled the greatest empire the world has seen.

Norway

Finally, let us turn to that exemplar of natural resource management and governance more generally. The IMF’s report titled “Counting the Oil Money and the Elderly: Norway’s Public Sector Balance Sheet” (Cabezon E., Henn C., 2018) has some useful insights. From the abstract:

“Unsurprisingly, we find that Norway’s current assets exceed its liabilities by some 340 percent of mainland GDP. But its nonoil fiscal deficits have grown very large (to almost 8 percent of mainland GDP) and aging pressures are only commencing. Therefore, Norway’s intertemporal financial net worth (IFNW) is negative, at about -240 percent of mainland GDP. As IFNW represents an intertemporal budget constraint, this implies that Norway’s savings are likely insufficient to address aging costs without additional fiscal action.”

What this means is that given the current budget stance, Norway’s public sector net worth will go from +340% to -240% of GDP, or a wealth reduction of 580% of GDP! From the main report

“Not surprisingly, our analysis shows that Norway’s static fiscal position is highly positive. Static public sector net worth for Norway stood around 340 percent of mainland GDP as of 2017, driven mainly by GPFG assets and the present value of remaining oil and gas deposits.

“Intertemporal financial net worth (IFNW) is our preferred indicator of long-run sustainability of current fiscal policies. Negative IFNW is an indication that fiscal policies will need to be eventually changed to fulfill the budget constraint. Negative IFNW could also provoke adverse financial market reaction, if agents’ confidence deteriorates that policy adjustment would eventually be undertaken in the future.

“But, more surprisingly, Norway’s intertemporal financial net worth (IFNW) is negative. Non-oil fiscal deficits have been rising steadily over the past 15 years. While they were less than 2 percent of mainland GDP in the early 2000s, they now stand close to 8 percent of mainland GDP. The rise occurred during a period of positive aging trends — but aging costs will now start to mount. Therefore, in a passive baseline scenario wherein deficits increase one-to-one in line with aging costs, Norway’s IFNW would be negative at close to -240 percent of mainland GDP.

“To put the IFNW magnitudes into more familiar terms, note that permanent savings of 1 percentage point of mainland GDP starting in 2024 would improve the intertemporal component — and thereby IFNW — by 60 percent of mainland GDP. Thereby, if a hypothetical one-time fiscal consolidation were implemented relatively soon, then savings of 4 percent of mainland GDP would be sufficient to bring IFNW to zero.”

By extension, if Norway wanted to keep its static net worth constant & sustainable in an intertemporal perspective, the total fiscal consolidation required would be nearly 10% of mainland GDP (340+240=580, 580/60 = 9.67% ~10%).

Conclusion

It is clear that we need to define some clear goals for public sector net worth. One basic goal is non-declining net worth, the essence of sustainability. Another obvious goal is for public sector net worth to be positive. The question is how high should the target be? 50% of GDP? 200% of GDP?

Read more:

Mitigating the Resource Curse by Improved Government Accounting: Goa Foundation’s note to the IMF and others explaining this issue, and how metaphors used are exacerbating the problem

FAQs on Accounting Metaphors: A response to various comments received to the previous note.

What is The Future We Need: a summary of our broader campaign. Highly recommended.

Stop selling the family farm: How the Arctic Refuge has been opened to oil drilling, partly due to this issue.

Alaska’s Budget Problem: How “revenue” accounting, commodity volatility and a fiscal rule that only 25% be saved in the Permanent Fund has caused the ongoing budget crisis that started in 2013.

Rahul Basu is the Research Director of Goa Foundation, an environmental NGO in India. The Future We Need is a global movement asking for natural resources to be viewed as a shared inheritance we hold as custodians for future generations. This work is based on the practical work of the Goa Foundation.